Three things to take away

What is the outlook for the UK’s marine sector – and how is the geopolitical and economic landscape impacting growth

What are the major risk areas for marine firms in 2024

What can marine firms do to mitigate risk, meet policy regulations and promote growth

The marine sector remains critical for UK companies including those that rely on ships to import and export goods, or to transport passengers. The effects of both Brexit and the conflict in Ukraine continue to impact maritime transport and those operators reliant upon it, notably through supply chain disruption, sanctions compliance, and customs requirements.

Labour issues and regulatory pressures will place additional pressure on maritime routes and supply chains, while the environmental impact of the marine sector will increasingly become a focus point for tightening regulation, requiring a balance between sustainable goals and commercial realities.

What is the outlook for the UK’s marine sector – and how is the geopolitical and economic landscape impacting growth

What are the major risk areas for marine firms in 2024

What can marine firms do to mitigate risk, meet policy regulations and promote growth

The marine sector remains critical for UK companies including those that rely on ships to import and export goods, or to transport passengers. The effects of both Brexit and the conflict in Ukraine continue to impact maritime transport and those operators reliant upon it, notably through supply chain disruption, sanctions compliance, and customs requirements.

Labour issues and regulatory pressures will place additional pressure on maritime routes and supply chains, while the environmental impact of the marine sector will increasingly become a focus point for tightening regulation, requiring a balance between sustainable goals and commercial realities.

Introduction

The marine sector remains critical for UK companies including those that rely on ships to import and export goods, or to transport passengers. The effects of both Brexit and the conflict in Ukraine continue to impact maritime transport and those operators directly or indirectly reliant upon it. This is most notable through disruption to supply chains and trade flows, additional administrative burdens linked to sanctions compliance, and customs requirements for trade with EU markets.

Labour issues and regulatory pressures will complicate operations in the coming years, placing additional pressure on maritime routes and supply chains. Ports remain crucial nodes of UK supply chains but several strikes have affected ports in recent years, with resulting reduction in calls to those ports and vessels diverted to alternative locations contributing to congestion.

The environmental impact of the sector will increasingly become a focus point for tightening regulation, and for environmental campaign groups: in the past, direct action has targeted cruise ships or oil and gas assets and this is likely to be repeated. Businesses will need to respond to divergent stakeholder concerns, striking a balance between sustainable goals and commercial realities.

The marine sector remains critical for UK companies including those that rely on ships to import and export goods, or to transport passengers. The effects of both Brexit and the conflict in Ukraine continue to impact maritime transport and those operators directly or indirectly reliant upon it. This is most notable through disruption to supply chains and trade flows, additional administrative burdens linked to sanctions compliance, and customs requirements for trade with EU markets.

Labour issues and regulatory pressures will complicate operations in the coming years, placing additional pressure on maritime routes and supply chains. Ports remain crucial nodes of UK supply chains but several strikes have affected ports in recent years, with resulting reduction in calls to those ports and vessels diverted to alternative locations contributing to congestion.

The environmental impact of the sector will increasingly become a focus point for tightening regulation, and for environmental campaign groups: in the past, direct action has targeted cruise ships or oil and gas assets and this is likely to be repeated. Businesses will need to respond to divergent stakeholder concerns, striking a balance between sustainable goals and commercial realities.

The marine sector in the UK

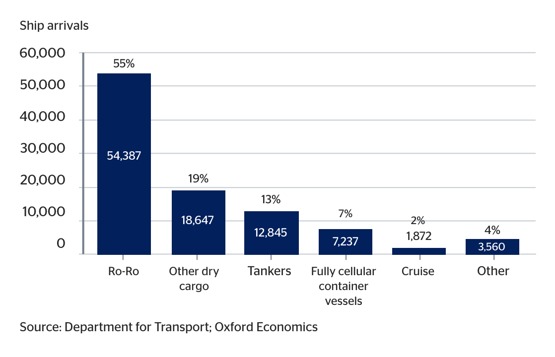

In 2022, a total of 98,548 commercial vessels arrived at UK ports. Over half (54,387) were roll-on/roll-off’ (ro/ro) ferries carrying both passengers and cargo from European destinations (Fig. 1).1

Dry cargo vessels carrying agricultural products (such as grain, soya, tapioca), coal, ores and other raw materials were the second most frequent arrivals with 18,647 ships docking (19% of total). Tankers carrying crude oil, liquefied gas and oil products ranked third, with 12,845 ship arrivals (13% of total).

A total of 14.3 million passengers passed through UK ports in 2022.2 Of these, 12.2 million were ferry passengers on shorter routes from Europe, mostly passing through Dover, Holyhead, and Portsmouth. Only 80,000 passengers travelled via longer routes. The remaining two million were cruise passengers, most of whom embarked or disembarked at Southampton.

1. Department for Transport. 2023. Table PORT0601: UK port ship arrivals, by vessel type and size of vessel, from 2009. Accessed October 2023.

2. Department for Transport. 2023. All UK international short sea, long sea and cruise passengers. Accessed October 2023.

Fig 1. UK port ship arrivals, by vessel type in 2022

The marine industry is economically important for the role it plays in boosting connectivity, bringing trade, tourism and energy to the UK.

In 2022, a total of 98,548 commercial vessels arrived at UK ports. Over half (54,387) were roll-on/roll-off’ (ro/ro) ferries carrying both passengers and cargo from European destinations (Fig. 1).1

Dry cargo vessels carrying agricultural products (such as grain, soya, tapioca), coal, ores and other raw materials were the second most frequent arrivals with 18,647 ships docking (19% of total). Tankers carrying crude oil, liquefied gas and oil products ranked third, with 12,845 ship arrivals (13% of total).

A total of 14.3 million passengers passed through UK ports in 2022.2 Of these, 12.2 million were ferry passengers on shorter routes from Europe, mostly passing through Dover, Holyhead, and Portsmouth. Only 80,000 passengers travelled via longer routes. The remaining two million were cruise passengers, most of whom embarked or disembarked at Southampton.

1. Department for Transport. 2023. Table PORT0601: UK port ship arrivals, by vessel type and size of vessel, from 2009. Accessed October 2023.

2. Department for Transport. 2023. All UK international short sea, long sea and cruise passengers. Accessed October 2023.

Fig 1. UK port ship arrivals, by vessel type in 2022

The marine industry is economically important for the role it plays in boosting connectivity, bringing trade, tourism and energy to the UK.

The marine sector’s contribution to the UK economy

The marine industry is economically important for the role it plays in boosting connectivity, bringing trade, tourism, and energy to the UK.

But it also makes its own contribution to the UK economy. Official statistics show that in 2021, 1,358 firms worked in the water transport sector.3 They employed over 15,000 people, or 0.1% of the total number of people employed in 2021.4 Of these, 85% were involved in sea and coastal passenger and freight transport, providing jobs in coastal communities where alternative employment opportunities can be rare. The sector made a £1.4 billion Gross Value Added (GVA) contribution to UK Gross Domestic Product (GDP) in 2021 (0.1% of total). Wider definitions of the shipping sector suggest it generated 61,000 jobs onshore or at sea.5

3. ONS. 2023. Non-financial business economy, UK: Sections A to S. Accessed October 2023.

4. ONS. 2023. NOMIS: official census and labour market statistics. Accessed October 2023.

5. Chamber of Shipping. 2023. The value of shipping: Delivering a prosperous UK.

The marine industry is economically important for the role it plays in boosting connectivity, bringing trade, tourism, and energy to the UK.

But it also makes its own contribution to the UK economy. Official statistics show that in 2021, 1,358 firms worked in the water transport sector.3 They employed over 15,000 people, or 0.1% of the total number of people employed in 2021.4 Of these, 85% were involved in sea and coastal passenger and freight transport, providing jobs in coastal communities where alternative employment opportunities can be rare. The sector made a £1.4 billion Gross Value Added (GVA) contribution to UK Gross Domestic Product (GDP) in 2021 (0.1% of total). Wider definitions of the shipping sector suggest it generated 61,000 jobs onshore or at sea.5

3. ONS. 2023. Non-financial business economy, UK: Sections A to S. Accessed October 2023.

4. ONS. 2023. NOMIS: official census and labour market statistics. Accessed October 2023.

5. Chamber of Shipping. 2023. The value of shipping: Delivering a prosperous UK.

Our central forecast is that the UK water transport sector’s

production (in real terms) will contract by 8.5% in 2023.

Ignoring the Covid-19 pandemic, this is the sharpest

contraction since 2016. This mostly reflects the decline in

the value of goods exported out of, and imports into the UK,

which are predicted to decline by 4.7% and 7.2% in the year.

Economic challenges facing the marine sector

Some marine companies have experienced volatility in the prices they have been able to charge over the last few years. The Covid-19 pandemic led to dislocations in shipping with port closures and passenger travel bans. This impacted freight and passenger transport differently. Freight transport companies experienced heightened demand as consumers switched their consumption towards goods. Manufacturers scrambled for inputs to meet the demand and ships to transport their supplies of raw materials. This led to the much publicised increase in container spot rates and profits for liners. In contrast, the Covid-19 pandemic adversely impacted demand for marine passenger transport.

One of shipping firms’ major expenses is fuel. Firms were therefore heavily hit by the steep increases in fuel prices sparked by the Russian invasion of Ukraine in February 2022. For example, output prices of UK fuel manufacturers increased by 66% between 2021Q4 and 2022Q3, before almost falling back to their pre-invasion levels in 2023Q3. Water transport companies have therefore faced a choice to pass the fuel prices increase on to customers and lower their margins - or increase their prices and risk a decline in demand. The Office for National Statistics data suggests freight and passenger water transport firms put their prices up by 15% and 11% between 2021Q4 and 2022Q3 and have largely left them unchanged since.

The three major container liners’ results presentations to investors all suggest the prices this segment of the marine industry can charge its customers will fall further over the next few years. This mainly reflects an increase in orders for new container vessels, which will boost supply when they have been built.

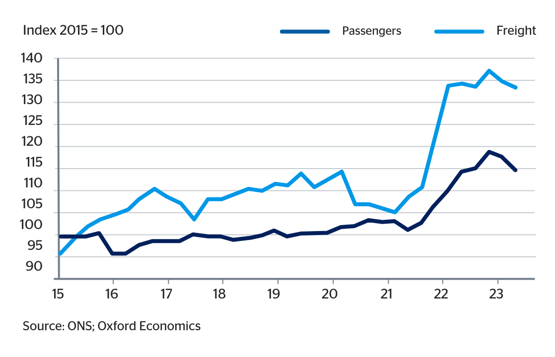

Fig. 2. Sea and coastal water transport output prices

As in other sectors, labour shortages are another factor that has often been reported by marine companies as being an issue. In the CBI Service Sector Survey for 2023Q3, 35% of marine and other transport firms surveyed reported that a shortage of professional staff would be likely to limit their ability to increase the level of business over the next year. Shortages of clerical or other staff was cited as a constraint on future output by 39% of all types of transport firms.

Some marine companies have experienced volatility in the prices they have been able to charge over the last few years. The Covid-19 pandemic led to dislocations in shipping with port closures and passenger travel bans. This impacted freight and passenger transport differently. Freight transport companies experienced heightened demand as consumers switched their consumption towards goods. Manufacturers scrambled for inputs to meet the demand and ships to transport their supplies of raw materials. This led to the much publicised increase in container spot rates and profits for liners. In contrast, the Covid-19 pandemic adversely impacted demand for marine passenger transport.

One of shipping firms’ major expenses is fuel. Firms were therefore heavily hit by the steep increases in fuel prices sparked by the Russian invasion of Ukraine in February 2022. For example, output prices of UK fuel manufacturers increased by 66% between 2021Q4 and 2022Q3, before almost falling back to their pre-invasion levels in 2023Q3. Water transport companies have therefore faced a choice to pass the fuel prices increase on to customers and lower their margins - or increase their prices and risk a decline in demand. The Office for National Statistics data suggests freight and passenger water transport firms put their prices up by 15% and 11% between 2021Q4 and 2022Q3 and have largely left them unchanged since.

The three major container liners’ results presentations to investors all suggest the prices this segment of the marine industry can charge its customers will fall further over the next few years. This mainly reflects an increase in orders for new container vessels, which will boost supply when they have been built.

Fig. 2. Sea and coastal water transport output prices

As in other sectors, labour shortages are another factor that has often been reported by marine companies as being an issue. In the CBI Service Sector Survey for 2023Q3, 35% of marine and other transport firms surveyed reported that a shortage of professional staff would be likely to limit their ability to increase the level of business over the next year. Shortages of clerical or other staff was cited as a constraint on future output by 39% of all types of transport firms.

Key things to watch

- Shipping and sanctions: While not ’new’, the impact of geopolitics for shipping – already seen in sanctions against countries including Iran and Venezuela – increased significantly with the conflict in Ukraine, and enforcement and the corresponding burden on maritime business to demonstrate compliance is set to continue. The coming years are likely to see the sector face scrutiny from regulators while adjusting to the shift in trade flows resulting from regulatory pressure and new trading relationships.

- Green goals: While meeting compliance requirements driven by geopolitical complexities, the sector will also continue to address its environmental footprint. An immediate impact will be seen in seaborne trade between the UK and EU, with maritime transport included in the EU’s Emissions Trading System (ETS) from 2024. Both intra- and inter-EU voyages are included. Across the UK, expect to see periodic targeting of offshore oil and gas infrastructure and vessels seen as high-polluting by environmental groups.

- Lingering labour challenges: Maritime workers have not been immune from those economic challenges that resulted in industrial action in other sectors. Strikes and workforce shortages will persist in the coming years. Looking to the longer term, maritime businesses seeking to attract and retain workers need to meet greater expectations around career aspirations, connectivity, and ensuring workers access emerging skills development.

6. What do Red Sea assaults mean for global trade? - BBC News

- Global supply chains: Disruption in the global supply chain can happen at any time. Currently, delays can be seen in the typically busy shipping lanes of the Red Sea, as many of the world's largest shipping companies divert their vessels away from the region. Alternative shipping routes may remove the risk of attack in the Bab al-Mandab Strait – but will add up to 10 days shipping time and cost millions of dollars6.

- Shipping and sanctions: While not ’new’, the impact of geopolitics for shipping – already seen in sanctions against countries including Iran and Venezuela – increased significantly with the conflict in Ukraine, and enforcement and the corresponding burden on maritime business to demonstrate compliance is set to continue. The coming years are likely to see the sector face scrutiny from regulators while adjusting to the shift in trade flows resulting from regulatory pressure and new trading relationships.

- Green goals: While meeting compliance requirements driven by geopolitical complexities, the sector will also continue to address its environmental footprint. An immediate impact will be seen in seaborne trade between the UK and EU, with maritime transport included in the EU’s Emissions Trading System (ETS) from 2024. Both intra- and inter-EU voyages are included. Across the UK, expect to see periodic targeting of offshore oil and gas infrastructure and vessels seen as high-polluting by environmental groups.

- Lingering labour challenges: Maritime workers have not been immune from those economic challenges that resulted in industrial action in other sectors. Strikes and workforce shortages will persist in the coming years. Looking to the longer term, maritime businesses seeking to attract and retain workers need to meet greater expectations around career aspirations, connectivity, and ensuring workers access emerging skills development.

6. What do Red Sea assaults mean for global trade? - BBC News

- Global supply chains: Disruption in the global supply chain can happen at any time. Currently, delays can be seen in the typically busy shipping lanes of the Red Sea, as many of the world's largest shipping companies divert their vessels away from the region. Alternative shipping routes may remove the risk of attack in the Bab al-Mandab Strait – but will add up to 10 days shipping time and cost millions of dollars6.

Macroeconomic risks to the water transport sector

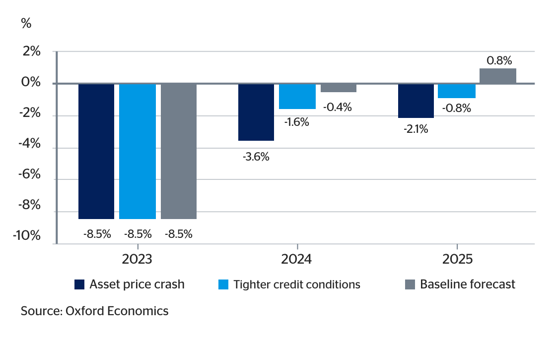

Our central forecast is that the UK water transport sector’s production (in real terms) will contract by 8.5% in 2023.7 Ignoring the Covid-19 pandemic, this is the sharpest contraction since 2016. This mostly reflects the decline in the value of goods exported out of, and imports into the UK, which are predicted to decline by 4.7% and 7.2% in the year.

Looking further out, the rate of growth of the water transport sector’s Gross Value Added is forecast to contract less in 2024, only by 0.4%, and is expected to grow by 0.8% in 2025. This reflects the strengthening in the UK and global economy, as household real disposable incomes begin to increase again, and interest rates begin to decline.

The water transport sector’s output is sensitive to cyclical developments. Its output is dependent on the volume of goods traded and passenger numbers, both of which are partly determined by the performance of the economy.

To look at potential risks to the sector, we explore what might happen to the water transport sector’s production under two more adverse macroeconomic scenarios using Oxford Economics’ Global Economic Model.8 Under the asset price crash scenario, the water transport sector’s contribution to GDP is expected to contract markedly, both in 2024 and 2025. This contrasts with the baseline scenario where we expect production to contract less in 2024, by 0.4%, and to increase by 0.8% in 2025. The tightening of credit conditions scenario, which increases the price and lowers the quantity of credit available, is forecast to lead to a smaller contraction in output over the next two years. Under this scenario, we expect output to contract by 1.6% and 0.8% in 2024 and 2025, respectively.

7. Oxford Economics. Global Industry Service. Accessed October 2023.

8. Oxford Economics. Global Scenario Service. Accessed October 2023.

The UK water transport sector’s production will contract by 8.5% in 2023.

Fig 3. Forecasts of annual growth in the water transport sector’s contribution to UK Gross Domestic Product, under different macroeconomic scenarios

Our central forecast is that the UK water transport sector’s production (in real terms) will contract by 8.5% in 2023.7 Ignoring the Covid-19 pandemic, this is the sharpest contraction since 2016. This mostly reflects the decline in the value of goods exported out of, and imports into the UK, which are predicted to decline by 4.7% and 7.2% in the year.

Looking further out, the rate of growth of the water transport sector’s Gross Value Added is forecast to contract less in 2024, only by 0.4%, and is expected to grow by 0.8% in 2025. This reflects the strengthening in the UK and global economy, as household real disposable incomes begin to increase again, and interest rates begin to decline.

The water transport sector’s output is sensitive to cyclical developments. Its output is dependent on the volume of goods traded and passenger numbers, both of which are partly determined by the performance of the economy.

To look at potential risks to the sector, we explore what might happen to the water transport sector’s production under two more adverse macroeconomic scenarios using Oxford Economics’ Global Economic Model.8 Under the asset price crash scenario, the water transport sector’s contribution to GDP is expected to contract markedly, both in 2024 and 2025. This contrasts with the baseline scenario where we expect production to contract less in 2024, by 0.4%, and to increase by 0.8% in 2025. The tightening of credit conditions scenario, which increases the price and lowers the quantity of credit available, is forecast to lead to a smaller contraction in output over the next two years. Under this scenario, we expect output to contract by 1.6% and 0.8% in 2024 and 2025, respectively.

7. Oxford Economics. Global Industry Service. Accessed October 2023.

8. Oxford Economics. Global Scenario Service. Accessed October 2023.

The UK water transport sector’s production will contract by 8.5% in 2023.

Fig 3. Forecasts of annual growth in the water transport sector’s contribution to UK Gross Domestic Product, under different macroeconomic scenarios

Advice for business

Maritime transport is inherently risky. One way to mitigate that risk is to thoroughly invest in staff training, so that all workers work as safely as possible in a productive way. Unfortunately, not all firms invest sufficiently in staff training; since 2020, only 0.2% of the maritime transport’s labour costs are spent on staff training.9

Another source of risk is technological hazards. These include engine issues, structural problems, failure of navigation equipment and other things that can go wrong with shipments or ships’ equipment. One way to prevent that, besides complying with global norms, is by hiring services from companies that specialise in inspecting and testing cargo ships and cruises. In addition, it is also necessary to keep all equipment up to date and to inspect ships before they depart.

9. UNCTAD. 2023. Review of Maritime Transport 2022.

10. What do Red Sea assaults mean for global trade? - BBC News

As detailed above, the maritime industry is buffeted by government policies across a broad range of issues. Keeping on top of sanctions and more stringent environmental regulations (such as the expansion of ETS) is important.

When possible, companies should also try to diversify their transport routes to lower risk from one-off events in particular countries. For example, the alternative shipping routes taken around the Cape of Good Hope and away from the Red Sea at present will drive shipping rates up (4% in the first week of attacks on commercial vessels10) and place the biggest delay on consumer goods.

Maritime transport is inherently risky. One way to mitigate that risk is to thoroughly invest in staff training, so that all workers work as safely as possible in a productive way. Unfortunately, not all firms invest sufficiently in staff training; since 2020, only 0.2% of the maritime transport’s labour costs are spent on staff training.9

Another source of risk is technological hazards. These include engine issues, structural problems, failure of navigation equipment and other things that can go wrong with shipments or ships’ equipment. One way to prevent that, besides complying with global norms, is by hiring services from companies that specialise in inspecting and testing cargo ships and cruises. In addition, it is also necessary to keep all equipment up to date and to inspect ships before they depart.

9. UNCTAD. 2023. Review of Maritime Transport 2022.

10. What do Red Sea assaults mean for global trade? - BBC News

As detailed above, the maritime industry is buffeted by government policies across a broad range of issues. Keeping on top of sanctions and more stringent environmental regulations (such as the expansion of ETS) is important.

When possible, companies should also try to diversify their transport routes to lower risk from one-off events in particular countries. For example, the alternative shipping routes taken around the Cape of Good Hope and away from the Red Sea at present will drive shipping rates up (4% in the first week of attacks on commercial vessels10) and place the biggest delay on consumer goods.

Lastly, cruise ships are subject to some unique risks, such as crowd control and crisis management issues, based on the large number of people on board. To ensure things go smoothly, cruise ship staff must be given the proper training to deal with a range of critical situations. One way to ensure staff members are trained while saving costs (e.g., transport) is to enrol in online courses that meet STCW (Standards of Training, Certification and Watchkeeping), which provide the basis for safety and people management.

After the stormy economic and political conditions that buffeted the UK maritime sector last year, the industry will likely find itself in the doldrums as 2024 and 2025 offer little prospect of growth on the horizon. The sector faces considerable challenges around pricing and sanctions, alongside geopolitical events, growing environmental concerns, and labour issues.

Lastly, cruise ships are subject to some unique risks, such as crowd control and crisis management issues, based on the large number of people on board. To ensure things go smoothly, cruise ship staff must be given the proper training to deal with a range of critical situations. One way to ensure staff members are trained while saving costs (e.g., transport) is to enrol in online courses that meet STCW (Standards of Training, Certification and Watchkeeping), which provide the basis for safety and people management.

After the stormy economic and political conditions that buffeted the UK maritime sector last year, the industry will likely find itself in the doldrums as 2024 and 2025 offer little prospect of growth on the horizon. The sector faces considerable challenges around pricing and sanctions, alongside geopolitical events, growing environmental concerns, and labour issues.

This report has been developed for QBE by Control Risks and Oxford Economics

This report has been developed for QBE by Control Risks and Oxford Economics

Building Supply Chain Resilience

Understand and manage risk in your supply chain

More like this

Sign-up to be notified about future articles from the Sector Resilience Series, and other thoughts, reports or insights from QBE.

Subscribe now